IRS Form 990 is more than just a tax form that many nonprofits must file every year. It’s an opportunity to demonstrate to the IRS, as well as to current and potential stakeholders, that your organization is well run and financially sustainable. It is also an opportunity to showcase key mission-centric programs.

Form 990 is another tool you can use to promote confidence in your organization and convince donors that funding your nonprofit will effectively support your mission. Read on for tips about how you can use Form 990 to inform and educate stakeholders of your organization’s accomplishments and financial health.

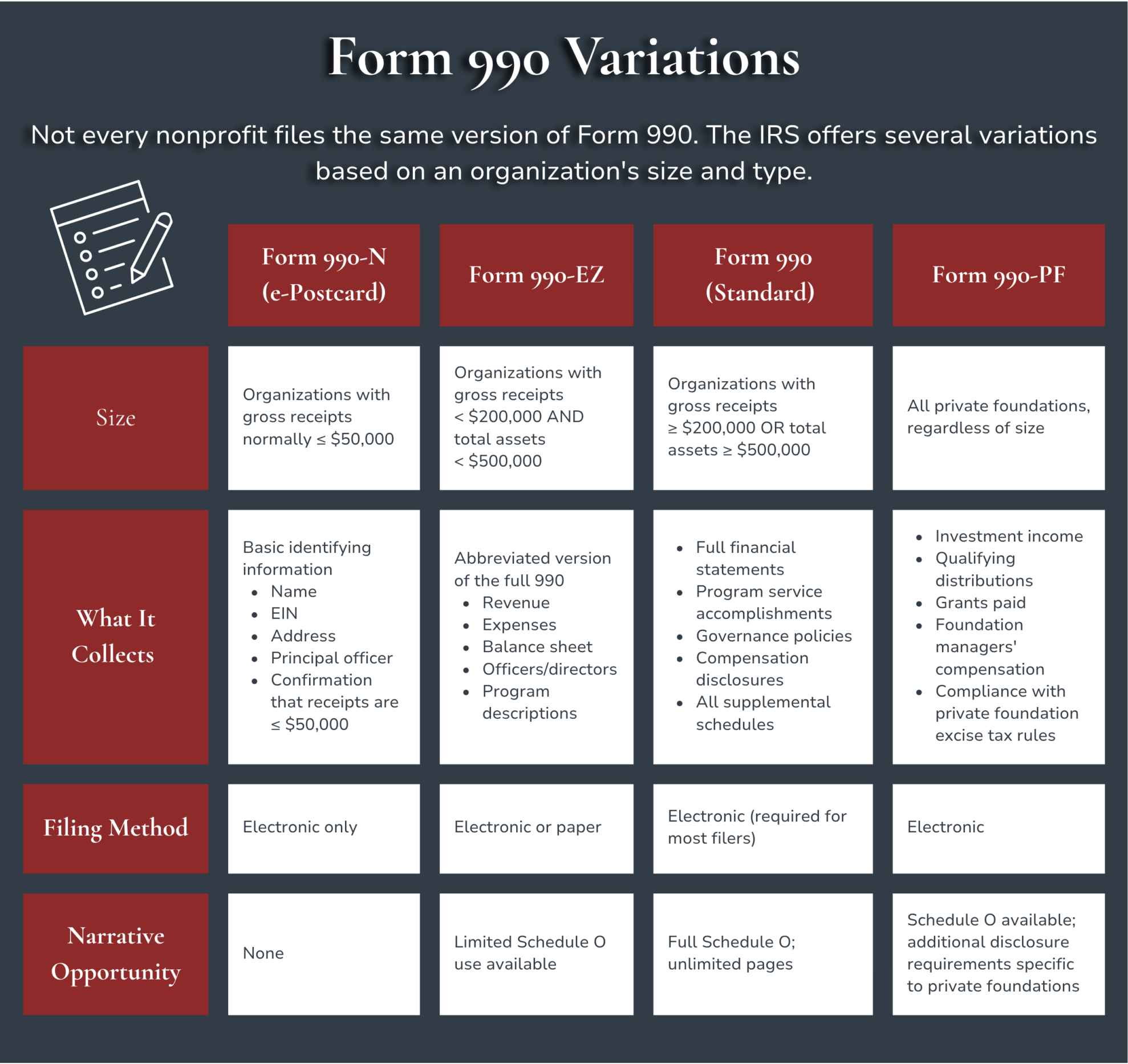

What is Form 990?

Most tax-exempt organizations that have annual gross receipts of at least $200,000, or assets worth at least $500,000, must file the standard IRS Form 990 on an annual basis. Some organizations, such as political organizations, churches, and other religious organizations, are exempt from filing an annual Form 990. Even though registered nonprofits are typically exempt from paying federal income taxes, the IRS still wants to make sure you are running your organization properly and in line with its tax-exempt purpose. Be aware that there are instances where your nonprofit may owe taxes if the IRS deems certain income unrelated to your tax-exempt purpose.

The 990 form is arguably the most important compliance requirement for nonprofits. The form has several purposes, including:

- Maintaining Your Tax-Exempt Status: The IRS wants to ensure you are not abusing your tax-exempt status and that your activities align with your organization’s mission.

- Overview of Your Organization: The 990 provides an inside look at your nonprofit’s finances, programs, and governance structure.

- Demonstrating Your Nonprofit’s Financial Strength: The 990 is an opportunity to demonstrate your nonprofit’s overall financial health to stakeholders so they can make an informed decision about whether to support your organization.

How Can You Leverage IRS Form 990?

The 990 form is a comprehensive document that includes your nonprofit’s financial information and details your organization’s mission and programs.

At the most fundamental level, providing detailed and accurate information for the following is valuable to the IRS as well as your stakeholders:

- Revenue: You will be asked to list your organization’s revenue sources such as income from donations and grants, membership dues, program services, and any investment income.

- Expenses: Another section of the IRS Form 990 requires you to list your organization’s expenses which include costs such as salaries, employee benefits, fundraising fees, and program expenses.

- Statement of Financial Position: An important component of the IRS Form 990 is a copy of your nonprofit’s Statement of Financial Position. You will list your organization’s total assets and liabilities to calculate your net assets.

- Compensation of Leadership: The IRS also wants to understand your organization’s compensation structure. That’s why the 990 form has you list the salaries of your nonprofit’s officers and directors, as well as key and highly compensated employees.

Take Advantage of Schedule O

The greatest opportunity, however, comes from fully using Schedule O. Nonprofits should use Schedule O narratives to address specific items on the IRS Form 990 and provide additional information that will be important to readers.

Provide additional information related to previous responses, such as:

- Explanations of the ratios of program expenses, general and administrative expenses, and fundraising expenses to total expenses.

- More detail about the organization’s mission, significant activities, and programmatic impact.

- Circumstances leading to a significant change in net assets.

An IRS Form 990 filer can use as many pages of Schedule O as desired, so do not shy away from sharing valuable information. Additionally, think about all possible readers, including current and potential donors and grantors, the media, watchdog groups, volunteers, and other stakeholders.

Selling Your Impact With Part III: Statement of Program Service Accomplishments

Part III is where many nonprofits miss a significant opportunity. This section asks you to describe your organization’s mission and three largest program services by expense.

While it may be tempting to keep descriptions brief, major donors, foundation officers, and grant reviewers read this section closely when evaluating whether to support your organization.

Use outcome-focused, specific language here. Instead of describing what your programs do, describe what they achieve. Rather than writing “we provide job training to low-income adults,” consider “our job training program served 412 adults in the past year, with 78% securing employment within 90 days of program completion.” Specific metrics signal credibility and organizational maturity. They also tell a story that a donor or grant reviewer can repeat when making the case internally to fund your work.

Using Compensation (Part VII) Transparency as a Trust-Building Tool

Many nonprofits approach Form 990 Part VII (Compensation of Officers, Directors, Trustees, Key Employees, Highest Compensated Employees, and Independent Contractors) with anxiety, fearing that disclosed salaries will invite criticism. In practice, the opposite is often true. Unexplained or seemingly disproportionate compensation raises red flags, while clearly contextualized compensation demonstrates good governance.

You can use Schedule O to proactively explain your compensation-setting process. Describe whether your board conducts an independent compensation review, whether you benchmark against comparable organizations, and how compensation aligns with your organization’s size and geographic market. This transparency signals that your leadership team is accountable to your board and your mission, which is exactly what sophisticated donors and foundations want to see.

Who Reads Your Form 990?

Once your Form 990 is filed, it becomes a publicly available document and is considered the go-to form for anyone looking to learn more about the inner workings of a specific organization. Form 990 serves as a credible, standardized source that people trust for information about financial health, governance, and mission alignment.

Major Donors and Foundations

Sophisticated individual donors and institutional funders routinely pull Form 990 before making significant gifts or grants. One area of focus is Part IX (Statement of Functional Expenses) , which allows them to assess how efficiently your organization allocates spending between programs, administration, and fundraising. They also review Part III (Program Service Accomplishments) to understand whether your described impact matches your financial investment and Part VII (compensation). All of which feed directly into your star rating with watchdog groups. A low rating on any of these platforms can suppress donations from donors who would otherwise support your mission. Keeping your 990 narratives clear and your financial ratios healthy directly influences these scores.

Board Candidates and Volunteers

Prospective board members and high-level volunteers may review Form 990 as part of their own due diligence before committing time and reputation to your organization. They look at Part VI (Governance, Management, and Disclosure) to assess whether your organization has sound policies in place, including a conflict of interest policy, whistleblower policy, and document retention policy. They also review compensation disclosures and financial trends to gauge organizational stability. A well-prepared 990 that reflects strong governance practices helps you attract the caliber of board talent your organization needs to grow.

Peer Nonprofits Benchmarking

Other nonprofits in your sector regularly review Form 990s from peer organizations to benchmark staff compensation, understand program expense ratios, and identify how comparable organizations structure and describe their work. Part VII compensation data is frequently used by nonprofits conducting salary reviews, and Part III program descriptions are studied to understand how leading organizations in a sector frame their impact. Your 990 is, in effect, a public statement of where your organization stands relative to peers, and it’s being read more than you might expect.

Journalists and Researchers

Investigative journalists, academics, and policy researchers use Form 990 as a primary source when examining nonprofit activity. A well-documented 990 with clear Schedule O narratives reduces the risk of misrepresentation and gives your organization control over how its story is told in any reporting

Common Mistakes That Erode Donor Trust

Even organizations with strong financial statements can undermine donor confidence through a poorly prepared Form 990. The following are some of the most common mistakes nonprofits make and how to avoid them:

- Leaving Schedule O Sparse or Blank: A bare-minimum Schedule O tells donors, foundations, and watchdog groups that your organization may lack the strategic awareness to use the form to your advantage. Use it to provide context for financial changes, explain your compensation process, and describe program impact in your own words.

- Using Vague or Jargon-Heavy Program Descriptions: Part III program descriptions written in jargon that is overly broad leaves readers unable to assess whether your work is actually effective. Replace jargon with specific populations served, measurable outcomes, and plain-language descriptions of your methods. Readers are evaluating whether your programs are worth funding, not whether you can write mission-statement prose.

- Inconsistencies Between Your 990 and Other Public Documents: One of the fastest ways to lose a grantor’s trust is to submit a grant application with program statistics that contradict what appears in your 990. Donors who do thorough checks will cross-reference your 990 against your annual report, website, and any grant applications. Discrepancies, even minor ones caused by different reporting periods or rounding, raise questions about data integrity. Establish an internal reconciliation process to ensure all public-facing financial data tells a consistent story.

- Misclassifying Functional Expenses: Overstating program expenses relative to administrative and fundraising costs may seem like it improves your financial ratios, but watchdog groups have become increasingly sophisticated at identifying misclassification. Unusually high expense ratios compared to peer organizations can trigger scrutiny. Classify expenses accurately and use Schedule O to explain any unusual ratios rather than masking them through misclassification.

- Not Disclosing Governance Policies in Part VI: Part VI asks whether your organization has a conflict of interest policy, a whistleblower policy, and a document retention and destruction policy. Many smaller nonprofits check “no” without realizing this can affect their credibility. Relevant audiences view these policies as baseline indicators of organizational maturity. If you don’t have them, creating them before your next filing cycle is a worthwhile investment — both for compliance and for the confidence they signal.

- Failing to Explain Significant Financial Changes: A significant drop in revenue, a large increase in net assets, or a spike in executive compensation without any narrative explanation invites speculation. Watchdog groups flag unexplained financial anomalies, and donors who notice them may simply move on to another organization. Use Schedule O to proactively address any year-over-year changes that might raise questions.

- Missing or Late Filings: Filing late signals poor financial management, regardless of the reason. Three consecutive years of non-filing results in automatic revocation of tax-exempt status—a recoverable but costly situation that damages donor confidence and requires IRS reinstatement. Build your 990 preparation timeline into your annual financial calendar and file for an extension proactively if needed rather than scrambling at the deadline.

When Must Form 990 be Filed?

Even though most nonprofit organizations are exempt from paying federal income taxes, organizations that meet the criteria noted earlier must complete IRS Form 990 and submit the document to the IRS annually.

An organization’s 990 form is due to the IRS five months and 15 days after the conclusion of the nonprofit’s fiscal year. For nonprofits that follow the calendar fiscal year, that date is May 15th (unless an extension is requested). If an organization fails to file for three consecutive years, they will have their tax-exempt status automatically revoked.

Final Thoughts

Your Form 990 isn’t just a tax form or compliance checkbox to complete each year. It’s a powerful, credible tool that attracts new donors, deepens trust with existing supporters, and builds confidence in your organization. If you need assistance compiling the information necessary to file your organization’s IRS Form 990 or could use some help with your nonprofit’s accounting in general, our team of expert nonprofit accountants can help! Reach out to schedule your free consultation.

Updated on 05/18/2026

Share This Post:

Chazin

With over 20 years working exclusively with nonprofits, we pride ourselves in having a unique understanding of nonprofit accounting needs. We believe that nonprofits deserve personalized, quality service and should not settle for a one-size-fits-all approach. We collaborate with you to provide a fully virtual and customized solution that is not only cost-effective but also strengthens your accounting function. We offer a team of industry experts at your disposal to provide advice, leading technology, and to supplement existing staff to improve efficiency and compliance.